Let’s optimize our costs

In order to be easily and correctly analyzed, the costs incurred by a business must first be classified. Cost analysis helps us to stay within the spending limits defined by our budget. For this purpose, we have created different cost categories in Budget-Mate but it is possible to create others according to specific needs. So our costs are divided into costs for raw materials, costs for energy, costs for transport, consultancy, personnel, financial and many others.

Production costs

Some of these costs thus classified are closely linked to the product sold and can therefore be considered to all intents and purposes production costs, or product costs, and as such must be considered to define the Gross Margin of our sales. To do this, in Budet-Mate, these costs will be inserted into the “account group” of the Gross Margin, also called the First Margin.

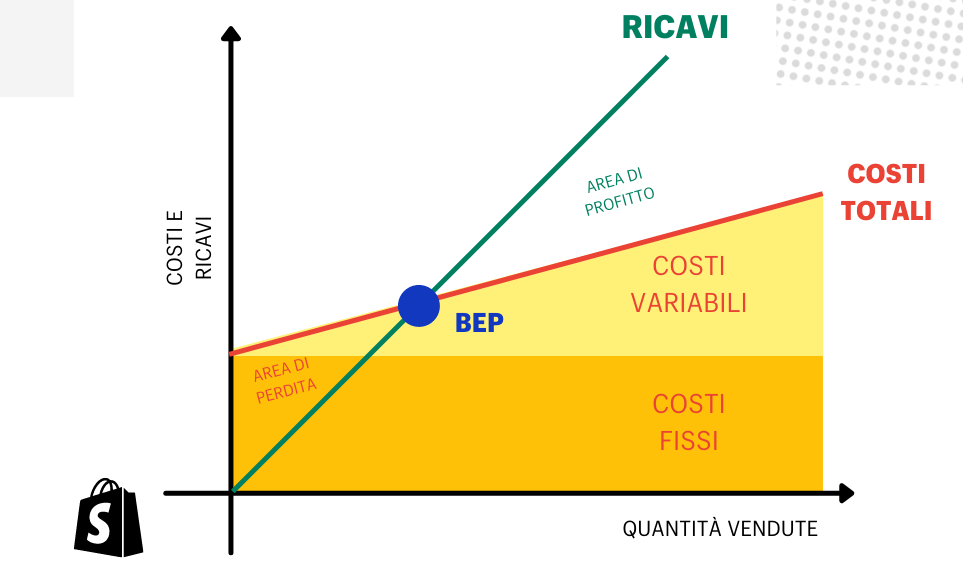

Variable costs and fixed costs

The costs that remain can in turn be classified into variable costs, where the underlying driver is sales volume, and into fixed costs which do not undergo appreciable changes when sales volumes change (within certain limits). This further classification in Budget-Mate is done by assigning the “account group” Variable Costs and Fixed Costs to these costs.

Urgent costs and important costs

But it is possible to go even deeper into our classification and assign a level of Importance and Urgency to each expense. Costs with high importance are those costs that are vital or are expected to produce an appreciable impact on our business, while those with low or medium importance are aimed at maintaining the current state. Urgent costs are those that cannot be deferred in time without generating penalties in our business. As can be understood, this classification, which is more subjective than the others presented, has three levels: high, medium, and low importance or urgency.

During the restructuring or cost optimization phase, it will then be easier to analyze fixed costs that also have low importance and low urgency. These types of costs can be drastically reduced without having major repercussions on our business.

And the Revenues?

What has been said for costs can also easily be applied to revenues with the obvious difference that the latter certainly does not need to be reduced but increased. We can therefore concentrate here on high-margin revenues, which will have in turn been classified as Important and Urgent.